With no limit to annual out-of-pocket costs under Original Medicare, many Pennsylvanians rely on supplemental coverage. Medicare Supplement plans in Pennsylvania help pay some – or even all – of your healthcare costs.

What is Medigap in Pennsylvania?

If you have Original Medicare (Part A, hospital insurance, and Part B, medical insurance), you can get help paying your out-of-pocket costs with a Medicare Supplement plan.

More commonly known as Medigap, these plans help pay for a variety of healthcare expenses. The plans are standardized, which means that Plan A provides the same coverage no matter where you buy it. The same is true for Plan B, Plan D, etc. At a minimum, all Medigap plans cover your Part A coinsurance and give you an extra 365 lifetime reserve days for hospital stays.

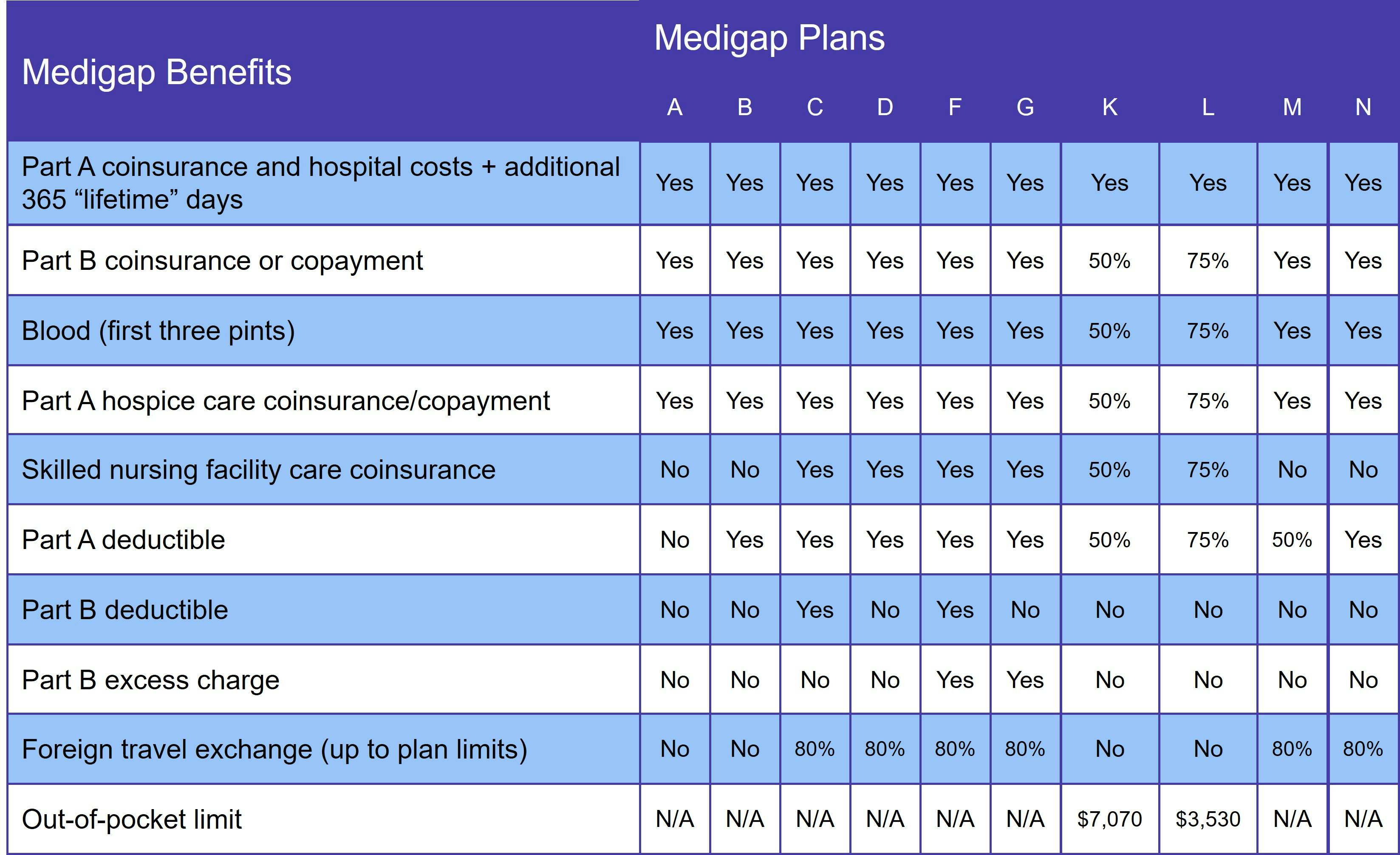

What does Medigap cover?

The level of coverage varies according to the plan you choose. The following table is provided to help you compare Medicare Supplement plan benefits.

There is no Supplement plan that includes prescription drug coverage. These benefits are available via Medicare Part D.

Who qualifies for Medicare Supplement Insurance in Pennsylvania?

Once you enroll in Original Medicare and are over age 65, you qualify for Medicare Supplement Insurance in Pennsylvania. In addition, state law also requires Medigap insurers to offer coverage to people who qualify for Medicare due to a disability, even if they are not yet 65.

When is the best time to join a Medicare Supplement plan in Pennsylvania?

The best time to enroll in a Pennsylvania Medigap plan is during your 6-month Medigap Open Enrollment Period (OEP). This begins the first day you are enrolled in Original Medicare. Although federal law only requires a Medigap OEP for Medicare beneficiaries who age into the program (i.e. are age 65 or over), Pennsylvania statute provides the same enrollment window for under-65 Medicare beneficiaries.

Your Medigap OEP is one of the few times you have a guaranteed issue right, which means your application will not go through medical underwriting. This is the process by which insurance companies determine whether to provide coverage and what your premium will be. When you have guaranteed issue rights, you cannot be denied a Medigap policy or charged more for it, even if you have preexisting medical conditions.

Medigap Plan C and Medigap Plan F in Pennsylvania

As of 2020, federal law prohibits Medicare Supplement plans from covering the Medicare Part B deductible. If you did not qualify for Medicare BEFORE January 1, 2020, you may not sign up for Medigap Plan C or Medigap Plan F.

Those who were eligible for Medigap before 2020 may join any plan, including C and F. However, that does not mean that they should. Once a Supplement plan is no longer available, premiums begin to rise.

With the exception of the Part B deductible, Medigap Plan D and Medigap Plan G provide the same coverage as Plans C and F, respectively.

How to choose a Medigap Plan in Pennsylvania

When deciding how much coverage you need, keep in mind that, unless you have a guaranteed issue right, your Medigap application goes through medical underwriting, even if you already have a Supplement plan. That's why we recommend getting the most comprehensive coverage you can afford.

Costs vary according to the provider you choose, so compare these carefully. Plans with an age-based premium will always cost more in the long run than those that use community rating.

Comparing Medigap plans in Pennsylvania is easy with our Find a Plan tool. Just enter your zip code to see Medicare plan options in your area.

Speak with a Licensed Insurance Agent

M-F 8:00am-10:00pm | Sat 9:00am-6:00pm EST