Original Medicare does not have an annual out-of-pocket limit, which is why most beneficiaries choose to supplement their coverage in some way. Medicare Supplement plans in Maryland help pay a variety of out-of-pocket costs, including coinsurance and deductibles. Commonly known as Medigap , some plans cover nearly every out-of-pocket cost you have while others mainly protect you against exorbitant hospital bills. The right choice for you depends on your unique situation.

What is Maryland Medigap?

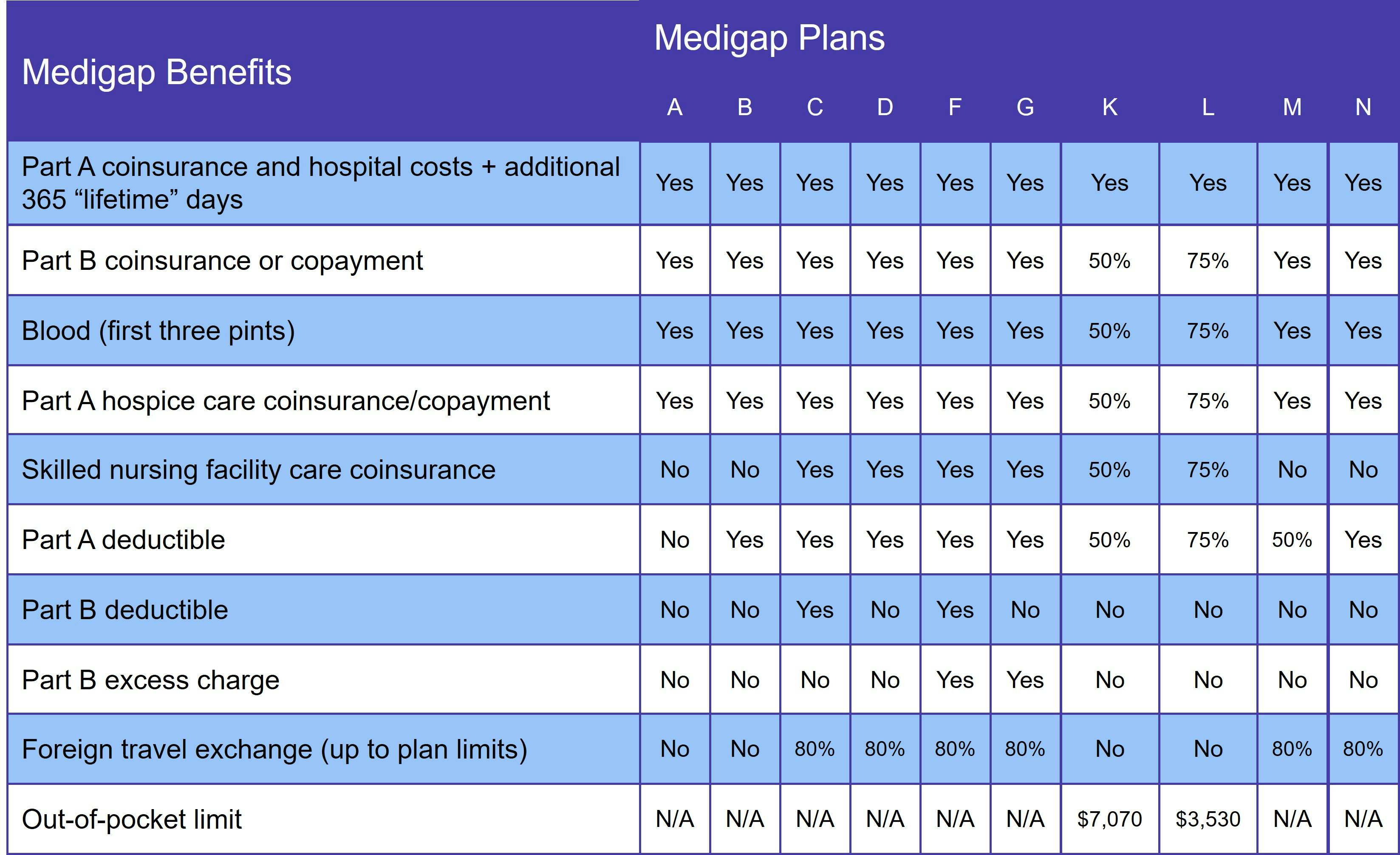

There are 10 standard Medicare Supplement plans available in Maryland (A, B, C, D, F, G, K, L, M, and N). However, not every Medigap insurer offers all 10 plans. In addition, some insurers provide high-deductible versions of one or more plans.

Each Medigap plan is standardized, meaning that you get the same benefits with that plan no matter where you buy it. While benefits are standardized, though, costs are not. Medigap insurers get to determine their own premiums, as long as they follow state and federal guidelines.

Unlike Original Medicare, you are not guaranteed access to a Supplement plan unless you have a guaranteed issue right. At all other times, your application goes through medical underwriting. This is the process insurance companies use to determine whether to sell you a Medigap policy and for how much. It involves answering a series of health-related questions, including age, tobacco use, and medical history.

Who qualifies for Medicare Supplement Insurance in Maryland?

At the federal level, you qualify for Medicare Supplement Insurance in Maryland as soon as you're aged 65 or older AND enrolled in Original Medicare. Most states also require Medigap insurers to offer plans to under-65 beneficiaries who qualify for Medicare due to a disability. This includes Maryland. The state enacted this requirement in 2017, after the passage of Maryland S.B. 48.

Maryland is not one of the states, though, that limit how much insurers can charge for a Medigap policy to under-65 beneficiaries. As a result, if you qualify for Medicare due to a disability and aren't yet 65 years old, expect to pay significantly more for a Medigap policy. However, once you turn 65, you get the same federal protections that other over-65 Medicare beneficiaries have.

What does Medigap cover?

Medicare Supplement coverage varies depending on which plan you choose. However, at a minimum, every Medigap plan pays the Medicare Part A coinsurance and gives you an additional 365 lifetime reserve days for inpatient hospital care.

The following table details which benefits each Medigap plan includes:

Please note that Medicare Supplement Insurance only covers services provided by Original Medicare. This includes Part A, hospital care, and Part B, medical services. It does not include prescription drug coverage. To get this protection, you need to join a standalone Medicare Part D prescription drug plan. There is a second option: signing up for a Medicare Advantage Prescription Drug plan (MA-PD). However, if you join an Advantage plan, you cannot also have Medigap.

Medigap Plan C and Medigap Plan F in Maryland

As of January 1, 2020, Medigap Plan C and Medigap Plan F are not available for new Medicare beneficiaries. This is due to a change in federal law that prohibits Supplement plans that pay the Medicare Part B deductible.

You can sign up for Medigap Plan D or Medigap Plan G instead. These plans offer the same benefits as Plans C and F, respectively, minus the Part B deductible. They also usually have a lower out-of-pocket overall, which is why we've been recommending Plans D and G for years.

When is the best time to join a Medicare Supplement plan in Maryland?

The best time to join a Maryland Medicare Supplement plan is during your 6-month Medigap Open Enrollment Period (OEP). It begins the day you enroll in both Medicare Part A and Medicare Part B. During your OEP, you have guaranteed issue rights. If you're age 65 or older, this means your application cannot be rejected. You also can't be charged a higher premium, even if you have preexisting conditions.

If you're under age 65, you're guaranteed a Medigap policy during your OEP. However, you may be charged a higher premium. You'll get a second Medigap Open Enrollment Period when you turn 65. At this point, you get the same protections as if you'd never had a Medigap plan.

How to choose a Medigap plan in Maryland

Since Maryland Medigap plans are standardized, the first step is deciding how much coverage you want. We recommend choosing a plan with the most comprehensive benefits you can afford. If you wait to join a Medigap plan with more robust coverage than Plan A, your application most likely has to go through medical underwriting. It may be impossible to get the coverage you need.

The next concern is pricing. Most Medigap insurers use one of three pricing methods:

- Attained-age rated: Premiums start out low but go up as you age. These policies usually cost the most over time.

- Community rated: Also known as no-age rated, since these plans charge the same premium regardless of age. Over time, these plans cost the least.

- Issue-age rated: Premiums are based on your age when you join the plan, not your age throughout the life of the policy. Rates may rise over time due to inflation, though.

Most Maryland Medigap insurers use attained-age and issue-age pricing.

Our Find a Plan tool makes it easy to compare Medigap plans in Maryland. Simply enter your location information to review Medicare plan options in your area.

Speak with a Licensed Insurance Agent

M-F 8:00am-10:00pm | Sat 9:00am-6:00pm EST