Since Medicare Part A and Part B, also known asOriginal Medicare, have no annual out-of-pocket maximum, it makes sense that many beneficiaries look to supplement their coverage. Florida Medicare Supplement insurance helps cover a variety of healthcare costs.

What is Medigap in Florida?

Medicare Supplement Insurance, also known asMedigap, helps pay for out-of-pocket costs related to Original Medicare. Medigap plans are standardized, which means that no matter which insurance provider you choose, the plans offer the same benefits.

Who qualifies for Medicare Supplement Insurance in Florida?

Any Floridian aged 65 or older who is enrolled in Medicare Parts A and B qualifies for Medicare Supplement Insurance. You may also sign up for a Medigap plan if you are under 65 but qualify for Original Medicare due to disability or illness. However, those under 65 tend to pay much more than those who are over 65.

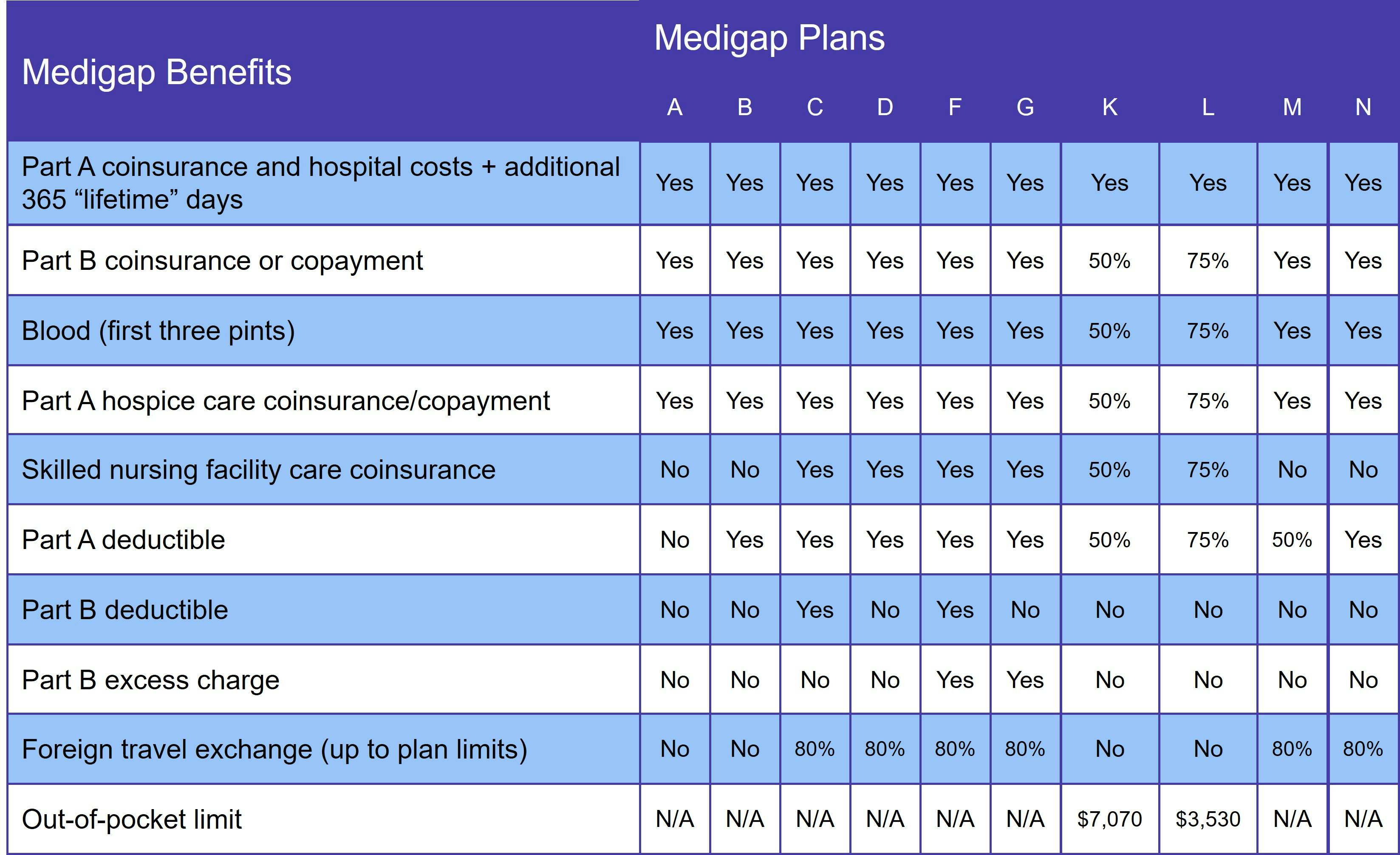

What does Medigap cover?

What your Medigap plan covers depends on the specific plan you choose. In general, you can expect your Medigap plan to provide an additional 365 lifetime reserve days of inpatient care and cover any Medicare Part A coinsurance.

The table below lists what each plan covers:

Supplement plans only pay for services covered by Original Medicare, so prescription drug coverage is not included. This comes from a Part D plan or a Medicare Advantage plan with drug coverage. But remember, you cannot have Medigap and Medicare Advantage.

Medigap Plan C and Medigap Plan F in Florida

You are ineligible for Medigap Plan C or Plan F if you qualify for Medicare on or after January 1, 2020. With the exception of the Part B deductible, you can get the same coverage by choosing Plan D (for Plan C) and Plan G (for Plan F).

When is the best time to join a Medicare Supplement plan in Florida?

The best time for anyone to join a Medicare Supplement plan is during their six-month Medigap Open Enrollment Period (OEP), which begins the day one is both 65 or older and enrolled in Original Medicare. This period is also one of the only times you have guaranteed issue rights and can avoid medical underwriting, which means your application cannot be denied and you cannot be charged more, regardless of pre-existing conditions you might have.

It is important to sign up during your OEP to ensure you get the comprehensive coverage. Otherwise, medical underwriting may prevent you from getting the protection you need later on. Medical underwriting involves asking a series of health-related questions (age, tobacco use, etc.) to determine whether an insurer will sell you a policy and what the rate will be.

How to choose a Medigap plan in Florida

Since the benefits of a plan are standardized, the main things to look out for are your needs and the cost. Be sure to compare multiple plans so you know you have the best possible plan for your medical needs. There are three pricing methods Medigap insurers may use:

- Issue-age rated: The premium is based on your age when you join the plan, with costs only rising due to inflation.

- Attained-age rated: Though premiums start low, they increase as your age does. Over time, this is the most expensive pricing method.

- Community rated: These plans charge the same regardless of age and are often referred to as no-age rated plans.

The easiest way to find and compare Medigap plans in Florida is with our Find a Plan tool. Just enter your location information to start comparing Medicare plans in your area.